In this episode, Zachary Beach of Wicked Smart Real Estate joins to discuss 2022 real estate opportunities with creative finance strategy. Topics discussed include the best exit strategy for creative finance deals, why sub2 deals help home buyers facing higher interest rates, and what an example subject-to or sub2 deals looks like.

Zachary Beach does a sub2 deal example walk-through and explains why subject-to is profitable. This podcast episode will run you through the basics of how creative finance works, who pays the existing mortgage, how sellers make money, and how buyers and investors get paid. Plus, if you’re thinking about entering the real estate industry and leaving your full-time job, you’ll hear how Zach built productive cold calling habits! This is a must-play!

Book a real estate coaching session with Bill Gross

Make sure you’re in our Facebook Group!

Probate Real Estate Certification Course

- Streaming Options

- Episode Segments

- Links and Resources

- Episode Transcript

- Get Certified in Probate

- Learn about QLS and grab the freebies from Wicked Smart Real Estate

Episode #66

Training Topics In 2022 Real estate opportunities with creative finance strategy: Lease Option, owner-financing, and subject-to deals

0:00 Zachary Beach: How I got started in real estate (Real Estate Motivation)

5:50 Lease option, owner-financing, and subject-to deals (Creative Financing)

9:23 How to take action and be successful in real estate (Real Estate Success)

14:36 2022 real estate opportunities: Learn creative financing (Real Estate Opportunities)

Get Certified in Probate Real Estate

17:08 Subject-To deals and banks due-on-sale clause? (Mortgage Liens)

25:18 Sample Sub2 deal example and exit strategy options (Transaction Engineering)

youtube.com/watch?v=bTg9P9DMD1U&t=2475s(opens in a new tab)

32:47 How do payments for sub2 deals work? Who pays the mortgage and who gets title in sub2? (Sub2 Deals)

35:24 Best lists to find motivated seller leads for creative finance deals (Motivated Seller Lists)

36:23 How to make more money as a real estate agent (Realtor Tips)

39:43 Learn creative finance free online; QLS course (Learn Real Estate)

Resources for this Real Estate Coaching Session:

- FREE TRAINING: Probate Fast Track

- Take Chad’s Probate Course and get Certified in Probate Real Estate

- Facebook Group: Estate Professionals Mastermind Group

- Alumni Group (For students of the Probate Mastery Course ONLY): Probate Mastery Alumni Group

- YouTube Channel

- Probate and Pre-Probate list providers

- Try Propstream Free

- Book a marketing strategy consultation

- Bill Gross’s Probate Weekly mastermind

- Recent content:

- Episode 65 Live Real Estate Coaching: Probate Leads and Transactions with Bill Gross (probatemastery.com)

- Probate Real Estate Role Play☑️Probate Cold Calling Objections: We’re getting so many letters and calls from other agents and investors!

- Bill Gross’s Website and Lead Vendors

- Learn more about QLS and grab some awesome creative finance freebies: http://smartrealestatecoach.com/probatemastery

EPISODE TRANSCRIPT How to grow your real estate business: Real Estate Referral Networking Ideas

Episode 66 of Estate Professionals Mastermind podcast

Zachary Beach: How I got started in real estate (Real Estate Motivation) [00:00:00]

Good afternoon, I’m bill gross. And this is a probate real estate call that we do every Tuesday at noon, Pacific 3:00 PM. Eastern everything in between I’m a graduate of the PR Probate Mastery program and one of Chad’s coaches, and a regular attendee on this call.

Also practitioner primarily in probate real estate. I’m excited today to have a guest. Zachary Beach is an expert really in helping us figure out how to invest in properties. I think that this program is about half investors and half real estate agents.

As a real estate agent or broker myself, it’s important to also build wealth by investing in real estate. And so there are times that make sense for us to step up our game and offer more service to the. As well as be able to deliver the value and deliver value maybe to ourselves as investors. Zach is going to explain kind of some options, some creative options, and financing that can take place for us.

So Zachary, welcome to our call.

Hey Bill! Thanks for having me. I’m excited to be here.

Thanks so much. Just a little background though. Where’d you grow up? I’m detecting an accent. You identified it before, where you grew up. How’d you get into real estate investing?

Yeah. I grew up in central Massachusetts, a town named town called Shrewsbury, right outside of Western mass.

So people that are from the New England area, know, I’m gonna speak fast. So please don’t ever hesitate to tell me to slow down. I got involved in real estate. I was a bartender and personal trainer down here in Newport, Rhode Island for–

..[ laughs] There’s a qualification for real estate!

Go ahead. I’m sorry to hear.

In Newport Rhode Island. After about four and a half years doing, you know, late nights and bartending and super early mornings at the gym, I then approached my father-in-law Chris PreFontaine who was just more or less re-inventing his real estate business right in 2008.

And previously before that, he was a broker-owner for 18 years and did fix and flips, raise roof projects, and condo conversions. But of course, like most people going up to 2006, and 2008, Personally signed and guaranteed loans because, if you pass the mirror of the fog test, they’d give you a loan.

So he was reinventing himself. So I went to him and said, Hey, I don’t know if I’m going to like real estate, but it’s going to be a lot better than what I’m doing right now. Cold calling on my breaks in between, and then eventually jumped into real estate full time. And now I’ve done hundreds of real estate transactions with little to no money down, not signing personally, not guaranteeing loans, spending all my time in the credit financing space, and now help people around the country build and scale their businesses by doing the same.

Fantastic. So as I touched a little bit, the first steps you’re making phone calls during your breaks. So you didn’t give it your full time nine to five, but you’ve managed a way to get some extra time in telling me about that a little bit in what we’re calling. Yeah. So, my schedule looked like this.

I would wake up at about 4, 4 30 in the morning and I’d hit my first clients’ training from about five to nine. So that’s about four clients and then I would have a break. So I’d take a power nap and then I would make cold calls to expired listings. I’m guessing that majority of you guys have an understanding of what an expired listing is, but, for those that are new, an expired listing is a listing that was on the market with the realtor or as a for-sale-by-owner at one point in time.

And for what, whatever reason it didn’t sell so expired. So in our book, those are fantastic leads because they’ve shown that they want to sell and they’re looking for other means of selling or other routes because the traditional market, for the reason I said wasn’t a good idea. So what we ended up doing is I make those cold calls and I was doing that for about an hour to two hours, starting at like 15 minutes.

And then I would do that for a couple of hours and then go take another power nap and then start bartending at like seven at night until two to three in the morning and then started all over again.

So for the new people that call expired listings were back in the days when we were younger, not every listing sold in like 10 minutes, and some listings didn’t sell. If you’re new to the market, I’m exaggerating a little bit. And there still are expired leads. Just not as many as it used to be, but they’re in a little more challenging, but there’s still there.

Sounds to me, kind of like people starting with a workout program that you had to build that muscle, that you weren’t Superman on the phones, that you had to work your way up to the cold calling. Describe that process of that.

Yeah, I’m glad you bring this up because the majority of the people that we train and partner with and buy and sell real estate with, they’re brand new to real estate, or they’re adding it, they’re new to real estate investing. It could be realtors and have that, that retail side.

But one of the biggest fears is the reluctance of picking up the phone. And the reason why most of us have reluctance on the phone is that we’re entering into something new and we don’t know what the other person on the line is going to say or ask us. And we don’t want to sound like idiots. So, that fear of not knowing what to say then comes into play, that imposter syndrome per se.

So now. When I first got started, I would just make phone calls. I would work with our scripts. I would see how far I could get into a phone call. At first. It was like a minute, they give you one rebuttal and you’re like, oh yeah, I gotta get off the phone. But then eventually you continue to move the needle forward.

And then you start to have a better conversation or ask better questions or speak less. And that takes time when it comes to real estate investing or communicating with sellers and buyers. And that is just spending more time asking the right questions and actively listening versus, verbal diarrhea of the mouth, in which we’re just constantly trying to tell people everything we know.

And most of the time that comes because we’re uncomfortable and we’re not sure about how to communicate yet. you know, We start at 15 minutes making a call or two, and then started to get some momentum. And then eventually you move from building this new habit of making phone calls. To now get yourself in a position where you’re determined on creating results.

Being an entrepreneur, being in real estate investing, we don’t get paid for the time we put in, we get paid for the results we create or the amount of value that we’re bringing by either buying a piece of real estate or helping a seller, or selling a piece of real estate by helping a buyer. And that’s when the transaction comes into play and we get paid for that.

That’s how I continue to build up and start going from behavioral time-blocking to what we consider results blocking.

Lease option, owner-financing, and subject-to deals (Creative Financing) [00:05:50]

In the beginning, when you’re calling expires, what were you looking to accomplish? Were looking to wholesale a deal or buy deals or investors, or what was your game plan for your first deal?

I remember my first deal was subject to deal. So we buy deals in different ways. The first is known as a lease purchase. Many people know it as a lease option. So we buy a lot of properties on lease options, really great way to get involved in the creative financing or the term space.

Because there’s typically a little to no money down a little to no risk because you’re not personally guaranteeing any debt. And you’re taking control of a piece of real estate. You’re not purchasing. To be able to then control that piece of real estate. And then we exit two different ways, which is via rent to own to our tenant-buyers or buyers that need time to qualify or we own or finance it to our buyers as well where now we’ve become the bank.

So lease option is number one, buying properties on owner financing, where the seller is the bank. Roughly a third of the properties in the United States are debt-free. Those are all fantastic prospects.

Some of these things we go by through quickly and it’s, and this is a very important piece of information.

People are. well, you really can’t do subject to, how often do you get a chance? Everybody has a mortgage.

One more time. Give us that statistic.

Yeah. About a third of the properties in the United States are debt-free. Yeah. And I did just hear and I can’t speak to it a hundred percent, but I did speak with some other people that buy seller financing in Canada who are telling me that it’s north of 50% of properties are debt-free across the border where I know it tends to be a little bit more difficult to get ahold of information based on, their laws. But those, properties are fantastic for seller financing, whether you’re north or south of the border there.

And then the last one that we buy or subject to deals.

So that means that you’re utilizing the current debt that’s on the property. You’re buying it subject to that existing financing. And. That was what my first deal was. My first deal was a sub2 deal.. So when I look for properties, we’re looking for those three different three main strategies.

We don’t wholesale. We don’t buy retail. We’re not typically your cash buyer either. We’re specifically looking to solve problems via creative financing. Because when my family reinvented itself and went back into real estate out of these new rules that we had to stick by, number one, to get back involved, which was not to sign on debt, not to raise large amounts of capital not to put down large down payments.

As we grew our business, it now went from rules that we had to live by to rules that we now choose to live by because why would we now go a different route if it’s been successful as we’ve come up throughout this process?

Because we can talk about, the shifting of the market and how that looks. But I mean, none of us are worried about none of our students are worried because we’re sitting in a very risk-averse position when it comes to all this.

Okay, so you start. How many, I’m sorry. I forgot the date.

How long ago was it that you started with the first deal?

That’s over seven years now. Seven years ago. And today, what does your business look like? Are you, I know you do some coaching. I know you do a financing or you do some and in your own business as well. What is it? What is your overall business look like?

Yep. So we have multiple seven-figure businesses, but one is specifically we have our buying and selling entity that I partner with my father-in-law and brother-in-law. We buy real estate up here in Southern New England, but then we also have a coaching company, smart real estate coach, where we teach people the exact model that we built with our business up here and now have people we’re in 80 plus markets now around the country in the trenches, helping people do deals.

How to take action and get results in real estate (Real Estate Motivation) [00:09:23]

I don’t coach investors. I try to help them because I come across investors as real estate brokers. I am an investor and, you know, I have a separate channel where I’m constantly interviewing different programs of coaches to encourage people to get started. What do you see as the one thing that holds people back from getting started, that you’re able to effectively get that, get that first deal going? So they get into action. People I meet the study, they go on calls. They go and bigger pockets podcast. They read books five years ago by them or buy anything. And they occasionally meet somebody who just jumps in and bought something. And then next thing they’re buying five and 10 properties.

What’s the difference? Or what’s the thing that gets people initiated started in your opinion? Well, it’s typically three things that we’ve discovered that hold people back from getting started in real estate. One is they don’t believe they have enough experience. Two as they don’t believe they have enough time or three as a don’t believe that, but no.

In all reality, a lot of those are just fears that are set up because if you knew you had the right system if you knew that that system could produce money and if you knew that you could manage that system or that business in the time that you have a lot. Right now, based upon juggling your family, your friends, your other business, or your W2, 95% of the people we coach have at least another job, if not another business.

And if you can manage all those and know that you could create a business that could produce which is our three payday system, create money now, cashflow monthly and backend profits, you know, anywhere from three to 10 years, then everyone would jump. Right. It’s just that here, everybody, everybody, everyone, we use this analogy and it’s, it’s an extreme analogy, but if you knew that, say somebody in your family was sick and they needed a million dollars and you need a million dollars to help them get a surgery, your urgency of creating that million dollars would happen overnight.

But when most of us think of our futures or our lifestyles, we tend to be able to procrastinate on that and the urgency isn’t able to be generated quick enough so then we never take action on the things that matter because we’re comfortable in this position that we’ve created for ourselves.

Yeah. I find it interesting that you started as a trained professional, a physical trainer. To me, it seems like it’s the same muscle, but it’s different, right? Like getting in exercising daily, there’s a certain discipline commitment. Some people just lock you in on that. So people work their way into it and lock onto it for the long run and other people will never get started.

And it’s the same in real estate or business. It’s a discipline and the commitment that you’re going to do this, no matter what. What I have to do as opposed to well it’s uncomfortable. Well, yeah, sometimes we’ll say it is uncomfortable. To describe a little bit then, so you mentioned the three things, in my experience I’ve been investing since 1986.

There’s never been more money available to brand new people. Everybody there’s just money gushing everywhere. It seems to me there’s never been more information for free with the internet. You can never keep up with all the videos being added, by some channels, let alone by the industry as a whole.

And so than the confidence, the knowledge that you can do it at some point, you kind of push people off the high dive to get them to jump in. So you have a program. I know you have a smart real estate coach program to help people get started. And the reason why you’re here is that Chad Corbett, who is an amazing teacher, who’s affected so many people’s lives, including my own knows that we need to be opportunistic when there are real estate opportunities for our clients.

We need to be opportunistic for ourselves So describe a little bit about the smart real estate coach and what you offer to help people get started, or people were in the business go from doing commissions for other people to making you money for their clients, as well as making money for themselves.

Yeah. The biggest thing when it comes to getting involved in real estate investing is knowing what information to follow and then implementing that information as well. You mentioned it a couple of times, which was, that there is so much information out there. We all can get information overload, which eventually we get a confused mind and we then don’t take action.

When it comes to exactly what we do, we have packaged a system that has been implemented in almost every single market across North America, effectively showing the results: that it doesn’t matter if we’re in a hot market, a cold market, or a flat market, we are solving challenges that every, that every market has sellers that are, that are facing.

In all reality, we have, we always have sellers. Doesn’t matter if we’re an extremely hot market of people that are behind on their mortgages. There are always life events that are happening with people. Doesn’t matter what market we’re in. We have sellers that do not want to access the traditional or retail market because they’ve just for whatever reason refused to pay commissions.

We see that all the time. Uh, We have tired landlords, especially nowadays, moratoriums are finally being lifted. We have this abundance of tire landlords that could not for the life of them. Get rid of the bad tenants that they had in their place there. Now we’re ready to sell, but they still have the dream of creating cash flow. Well, through creative financing, we can take over the property, and eliminate tenants, toilets, and trash.

And still, give them cash flow based upon the financials. One more time. Hold that, love that line. You could eliminate what slogan? Tenants, toilets, and trash. That’s fantastic with the accident. That’s just fantastic. So you have all of these, these different niches within real estate or these challenges that are within real estate.

2022 real estate opportunities: Learn creative financing (Real Estate Opportunities) [00:14:36]

And if you just knew how to communicate, know how to move property through a system, and then to be able to present deal structured options that not only create a win for you, create a win for your buyer, but then also be able to create three paydays on every deal that you do, that is what we supply.

We’re able to then be able to bring solutions to the marketplace. And I, I couldn’t say that there’s not a better time to get involved in this real estate niche based upon all the uncertainty that’s going on because this business was built upon uncertainty and we crafted it because we wanted it to weather, all storms, knowing that it’s gone through oh eight, it’s gone through COVID.

And now it’s about to go through this next cycle. One of the things that I want to bring up because I typically do it within our presentation. The media also stops a lot of people in their tracks. Two years ago the media told you not to buy real estate because of what? COVID causes COVID.

And then they said last year, don’t buy real estate because of what housing crisis, the market is too hot. Then this year they tell you don’t buy real estate because. So how you, we got a crisis on our hands and the market’s about to crash. So the way we’ve set up our business is to be able to navigate and weather those storms because we don’t have a mass amount of debt that we’re personally guaranteed on.

We’re not going and raising a bunch of capital and we don’t have a bunch of bank loans out there. So it doesn’t matter what the market does and how it shifts. We just continue to remain in these deals and create our cash flow

I’ve been saying this every week for the last two and a half years, there’s never been a better time to be involved in real estate to create income or wealth.

And it gets better every week because there’s more uncertainty. And if you have certainty, you can navigate the market where other people can’t. So look for those new to the call this is a close friend of Chad’s and his family’s close friend of Chad’s. They do business together. It’s because we’re already talking to families about the property.

If you’re prospecting, either talking to families or attorneys, you’re already in the hunt, you’re already close to the deal. You’re already in the marketplace. And this is just another tool for your toolbox. Whether you offer it to the client to disclose the property or be opportunistic when it’s appropriate.

And I understand I’m a broker you’d be appropriate about these tools appropriate to take advantage of them, yourself as an investor. When the position, when the opportunity presents itself, here’s a chance to talk to a master coach. WHe’sdone hundreds of these deals within his team, his own business within his team of coaching. Feel free to raise your hand if you’re on the zoom call or put a question in the chatbox.

Subject-To deals and banks due-on-sale clause? (Mortgage Liens) [00:17:08]

The first question I want to handle a little bit the question since I’m old school. I am also in school. It used to be legally possible to take overloads subject to how. He’s saying this changed decades ago. Why are investors concerned about banks calling loans due because of the ownership transfer? He doesn’t. Understand.

So first off, is it true that you can no longer do subject-to deals because banks always call the loans due?

You can do subject to. We do them consistently. The due on sales clause is a contractual agreement between the seller and the bank, it’s not illegal, but it’s not like you’re committing fraud.

You’re not doing anything illegal. It’s not a crime, it’s not a crime. It’s a simple contract between the owner of the loan and the bank, but it’s not a crime unless you mislead people. It’s not a crime to buy the property in the circumstances. Yup.

Absolutely. So when it’s appropriate, you buy these properties subject to, because you’re typically helping sellers out from a financial bind where they may not be able to make their mortgage payments or they may be in arrears.

And now you be able to, now you can help the sellers protect their credit and be able to move on. It’s a huge benefit that we help out sellers with, especially when appropriate. Now, there are many different ways to paper, these agreements in order to significantly lessen the likelihood of a due-on-sale clause being called.

I have never seen one called we had a a good friend of ours that was in Pennsylvania and his attorney simply said to him, Hey there’s some local banks calling some loans. Do what we’re suggesting is we do a contract for deed instead. So just another way to. Possession or ownership of a property is just another way to pay for it.

And I’m not going to go into a long conversation on contract deeds and land contracts, but just know there are so many different ways for you too, in order for you and your attorney to go ahead and paper these agreements. So that way you can help out the seller and you get the benefit of ownership.

So when was the way you pay for it? There’s also an insurance program. I believe that you can get that will cause this. Yeah. That’s like a whole new industry, right? So I have clients who are big-time wholesalers and that’s what they do in these sometimes, sometimes is they’ll tell the seller they’ll pay for it.

It comes out of the profit or comes out of the deal somehow, but there’s ways to do that as well. So these are being done. And, and I think that’s the key thing is we can always find excuses not to do anything, but when you’re committed, you want to fight an excuse to get the children. Then you find some way around all that that’s legal, ethical, and effective.

To help declare. Right. And so how many deals do you do subject to something or some format of a subject to how many are you doing in the last 90 days or within your cohort? We tend to do more sub2s now than when we first started our business, because it is a more advanced technique. When it comes to purchasing properties, I would say it’s like one to two out of every 10 ends up being a sub2 deal.

We’re now doing more sub twos with a seller carry, meaning that there’s equity in the. Because of the way we’re structuring, we would rather take ownership even if there is equity versus doing one of our other techniques, which is the lease option, which tends to have equity in a mortgage. So we’re doing these quite often.

Let me say this because I know that we’re, we’re trying to talk about an entire industry in about 45 minutes with some questions or things that, have taken me years upon years upon years to, to be able to. I break down and understand communication. And that’s, that’s exactly why we teach this and get in the trenches with people so we can help you implement it.

Right. But the other piece is you can always look for reasons why it doesn’t work and then you can always do look for reasons why it does work. And the reason why. Creative financing is such a magical place in Chad corporate said it too. Last week. We had them on our kind of similar sit-down here that we have to our audience.

Any said this you’re running in a different direction from everyone else. That’s why we’re able to create significant profits in our deals and help out both buyers and sellers. Nobody is willing to take the time and the effort to learn these techniques to get these things done, they would rather run in the similar position, which I’m sure you’re hearing, especially those are in the realtor space, wholesale space fix, and flip that there are no deals, deals aren’t viable.

A Marcus. We’re still doing deals. We still have these creative financing deals where terms that you would, that most people ask us, why sell would ever do that? And it’s because we’re providing solutions to people that other people don’t know how to do, or they’re not willing to learn how to do so this continues to bring that advantage to the table for you.

It doesn’t matter what industry you’re in or what market. Right. Yeah. There’s a phrase here, right? To the sound of the gunfire, the cows run away, but people committed to the cause we’ll ride towards it. I’m in real estate one way or the other. I’m talking to people every single day. And I would say the investors, I deal with find a way to work these things out.

And when they work it, they work it and work and work it over and over again and make a lot of money. I, again, this is Zach beach. He’s a smart real estate coach. In his father-in-law’s view, we’ve heard Chad referred to Chris Prefontaine. And so Zach is married I guess, to Chris’s daughter and they haven’t been good enough terms, but he’s here on the call.

The smallest space, I guess, would be a pretty good Zachary coach, a smart real estate coach, which is a program that helps people learn how to invest. And again, whether you’re talking about helping your clients do these programs, I imagine it’s hard to learn a one-off and have the confidence to do it, but more important.

As an investor or Russell broker comes across, these deals take the opportunity to make the income, make the asset that you went to for your family that you want to do with that. And I think that’s the key. Steve says that we have to start with value if we help other people out with their problems.

These are just some ways to do that. That traditional real estate may not get there. Okay. Are you flipping the question is, are you flipping a subject twos? I don’t see such to working for Elisa. I think not. If you’re able to get the deal paper properly, you have nice cash flow. Why would you ever flip it?

Forever right.

So our primary two exits are rent to own or we would utilize what we consider a wrap mortgage to now sell the property. And we’re now the bank. We are exiting a majority of our deals. I would say 95% of our deals with these verses are long-term buy-and-holds. And that’s just because we have made a conscious decision to not be landlords.

When we sell our properties to our buyers, They are treated like act like homeowners. So we’re not getting calls in the middle of the night. If the toilet’s not working or the fridge is broken, we’re passing along all of the responsibility to our buyers. And we are simply collecting a monthly check and helping somebody.

Cause we have a very systematic process to help somebody go from being unable to qualify for a loan today, to then being able to qualify for it. And we have a very high it’s over 90% completion ratio with our buyers. And right now and I’m sure you guys can all allude to it. Bill, you’re in sound like you’re in the retail space.

As the interest rates are rising by the droves buyers are now unqualified to become homeowners based on their DTI. Cause the interest rate all of those buyers now become fantastic rent and own buyers for us because all they simply need is time. And now we’re being able to provide our buyers with housing.

They come in with a nice non-refundable deposit. Which is anywhere from three to 10% down we then are collecting monthly cash flow from them. They get to live in the home, take care of the home and then work on becoming qualified for their loan. Once they qualify for the loan, they then just go ahead and pay us out.

And it makes sense for that buyer in that given most projections say nationally, the appreciation will slow down to only 11%, according to Zillow at the underlying interest rates of five or six. The house is still appreciating faster than the underlying debt. So they are going to build equity, not as much as they would, like, not as much as if they bought it all on the road.

But they can’t qualify. That’s not an option. That’s off the table. You’re giving them an option to get in the property, get the house they want, get the family into schools or whatever their issues are, and get started on that first property. That’s a fantastic program.

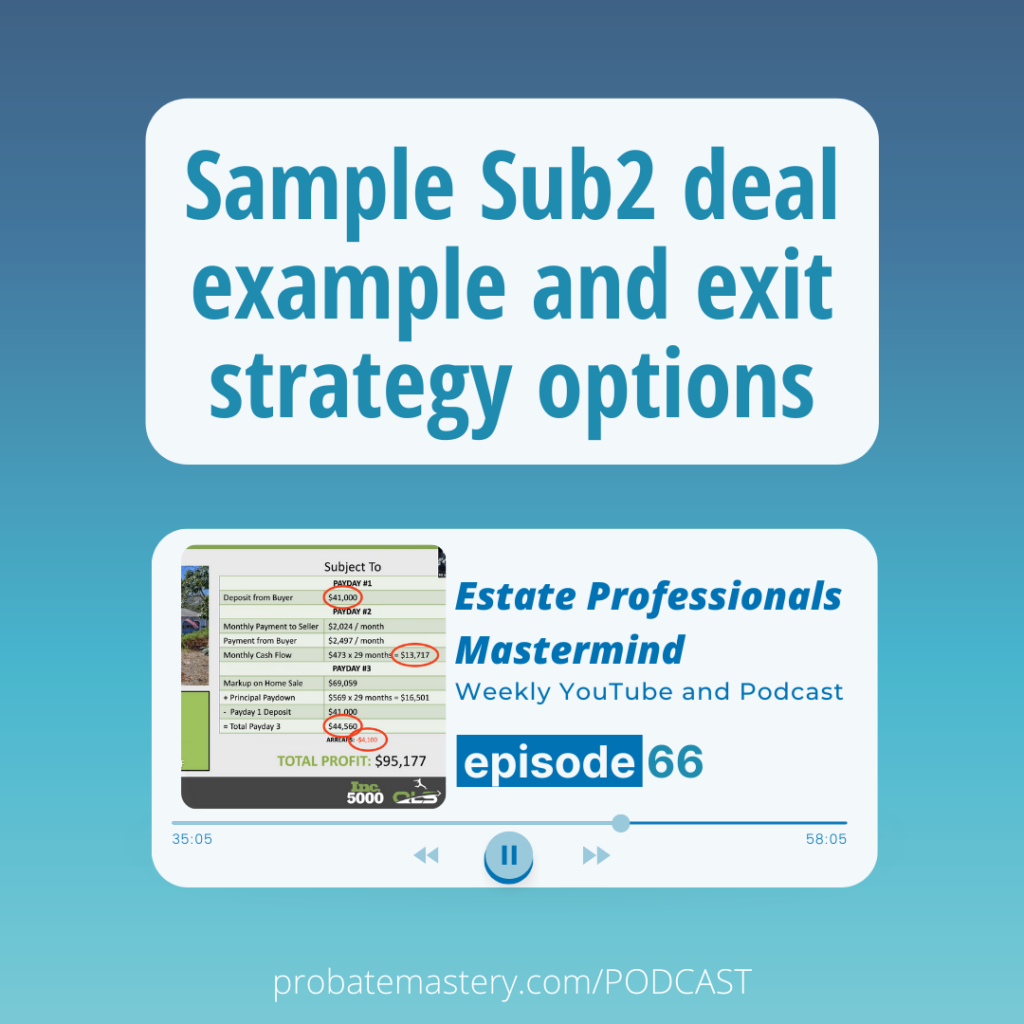

Sample Sub2 deal example and profit spread (Transaction Engineering) [00:25:18]

So Nina asks, can you round up, if you’re able to, can you run through a sample sub2 property walkthrough from approaching the owner of the property, through the disposition. Are you able to walk through that? We’ll only have another 30 minutes to go. Is there a five-minute version or three-minute version overview through the mechanics? Yup. Just give me one second here in ASA. Share my screen and run through a deal with you guys.

Let me just make sure I got the right one up here in front of me and I’ll run through a deal if you just give me two seconds. Okay.

Uh, Everyone sees this? Yes. Awesome. Well, here’s a sub-to deal that we did at the Cape. I don’t know if anybody knows familiar with the Cape, but it’s a place right out in Massachusetts around the water, a tourist-driven area. We bought this property in a sub2 installment. These buyers were in the process of getting divorced.

The wife was on both the title and the mortgage and the S and the husband were only on the title. So as soon as we closed on it, we only had to deal with it. These people racked up a bunch of credit cards they’re getting together and they decided to rehab a property utilizing a Home Depot loan, a Home Depot credit card, which I not advise.

Uh, So the reason why we created the installment sale is we were trying to help them solve their problem with some of their credit card debt.

So we purchased this property for $355,941. We sold it for $425,000. It was originally on the market for 425 for one reason or another. It didn’t sell.

So we went and put it back on the market again for 4 25. We sold this property as a lease-purchase with the option for owner financing. So that’s, this is a technique that we use. We sell it rent to own first to our buyers. And if we can finance them we could potentially do so, but we want to make sure that their nonrefundable deposits are coming in on time.

The rent’s coming in at a time before we transfer the title. And we usually do that over a two to three-year period. So we’re looking at our payday one here, which is our non-refundable deposit from our buyer. And that was $41,000 down. So just about 10% of our monthly payment to the seller’s bank is 20, 24.

So that’s P I T I. The payment from our buyer every single month is 24 97. Does that mean we’re getting a 4 73 spread? These are based on the 29 months of this deal. Uh, It’s probably going to go longer, but we want to be conservative in the projections for you. Uh, So that’s 13,750 on our payday two, which our payday twos are, is our cash flow on this property.

Our payday three is the, not as the premium that we sold the house for. So we bought it for 3 55. We sold it for 4 25. We also include our principal. Paydown. So out of this 24 97, 560 $9 as we make the monthly payment to the mortgage is coming directly off of principal is reducing the principal balance.

So over the 29 months at $16,000 in equity that we’re building into this deal, we already collected 41,000. So that means our backend total profits for payday three there’s 44,000. This property was in arrears for 4,100. They were about to go on their third payment. So we went ahead and paid that payment up.

So if you add up our three paydays on this deal, it’s 95,177.

And so when you bought the property, it was expired listing. You paid 3 55. You have, you already had the buyer through some sort of marketing. We have buyers who are looking all the time and you were able to pick when maybe I have a list and say, Hey, we have something for you might be a suit.

Or how did that work? Yeah, we’ve grown a list over time. The way we approach the buyer side is different than say wholesale deal. We don’t go look and acquire a large buyers list. First, we acquire the properties, and then based on the area and the property, our tenant-buyers are attracted by our marketing.

Then over time we have a larger list. These buyers, it took us about, I don’t know, I think it was like 30 days. It’s in a great school system to fill this property And so these buyers, basically, they’re responding to a rent to own or lease to own type situation. They put down less than 10%, the payments 24 97, which is probably maybe a little more than the rent, but they own the house or they, in their mind, they’re going to own the house that they want in the area.

And they have a plan to get there. And as long as they deliver, you’re, you’re glad to deliver children in those terms. Right. You can be happy to understand handed back to them and get your payments. And this was a subject to the, that the purchase of 3 55. Yeah. The purchase of 3 55 included. It was the exact mortgage balance plus it was, I think it was two payments of $5,000.

That’s what we call the install. How we paid $5,000 the following year after we closed on it. So we paid closing costs on the 4,100, the following year $5,000 was due. And then the following year after that $5,000 was due. So we spread out the installment over two years, even after we took pedal.

So you were like. Treating this spread the spread on those payments, like a lease option, if you will, that’s interesting. And with that, I just wanted to clarify the cash flow, were you giving any credit to the tenant buyers towards their purchase, or was it only their option fee was their only credit?

The ladder the monthly. It does not. None of it counts is credited towards the the purchase, only the non-refundable deposits count towards the purchase. This is something that we worked on with a mortgage lender and it is something that we do differently than most of the other industry does in the rent to own space.

And because it’s nice and clean between just non-refundable deposit and then just our mortgage lenders are able to qualify them more quickly instead of trying to go through the red tape of figuring out what is the current rent in the area and how much of that can they actually qualify for the bank loan to be credited for their purchase price.

So we don’t, we don’t go there. We don’t go that route. And then secondly, if we were giving them a large amount of credit on their monthly payment that does not incentivize them to go get their loan. Right. That actually does the opposite.

Exactly. And with the loan did, did not all lenders will do it, but did the lender allow for their option fee to be used for their down payment?

For all of our deals, the lenders can utilize them. So it’s not an option fee on our end. It is a non-refundable deposit that does get credited off the purchase price.

Okay. In California, we referred to it as an option.

As long as your mortgage lender is utilizing the same way that what I’m communicating here, then you should be able to help your buyers be able to qualify for loans significantly more quickly.

Because what we want to do is consistently increased their nonrefundable deposit or their option fee. So that way, when they go to get a loan, they don’t have to come out of pocket any more. And that way they can just go ahead and qualify for that loan. Now, in this case, your seller, who, who was trying to get a 4 25 and gave up and sold it for 3 55, they’re getting $2,000 a month, which I imagined covers our mortgage.

Are they getting, are they getting that’s more than their mortgage? That is exactly their mortgage. Like what’s in it for them. What are they getting out of the deal that they’re willing to pay to sell it for that price? Or they’re just getting out from under and they’re happy to get out from under it?

These particular people are just trying to get out from under it.

We pay and it shouldn’t say to the seller, that might be a little confusing.

How do payments for sub2 deals work? Who pays the mortgage and who gets the title in sub2? (Sub2 Deals) [00:32:47]

We pay everything directly to the bank. Right. For this reason, we don’t want to have to police and make sure, especially as we do more and more deals and make sure that your seller is now depositing the money to the bank or the mortgage lender.

You want to pay it directly. You want to have online access to that mortgage. You want to be able to, you want to be a part of either the authorization to release, which would be a document that means you can always get authorized to get any information in regards to that mortgage or be a limited power of attorney on that property, that way you can continuously make decisions on that mortgage because if you don’t, you put yourself in a bit of a liability position and also it doesn’t put your buyer in a great position either as you can see, they got 10% in this house. And we need to do everything in our power to control this process to make sure that they can be successful homeowners.

And one of the things I’ve learned is at the time, the buyers are willing to agree to the strictest terms, you can negotiate if you can think of it, to protect yourself. The problem is when you don’t get those powers upfront, it’s very hard to get back control of the property and the laws all go against you.

Then I’ll go in favor of the tenant slash rentee whatever. That’s the beauty of your system. You guys have been doing this for a while and worked out a lot of those details.

Terry’s got his hands up. Terry Peterson. How can we help you today? Yeah. I’m curious about your sub-to transactions, a couple of questions.

Are you sending all your sub2s up with the servicer, a mortgage servicer to handle the payments, and so forth? We are not. Okay. As well, do you ever, do you as an exit strategy, do you provide owner financing, a wrap mortgage, if you will, to the end buyer and, then as an exit, potentially sell that note at a discount?

We, in that particular deal, the real exit is going to be, because of the seller. I mean, the buyer has not reached that 30 months yet. But the option is on the table for us to finance that buyer. And now the interest rates increased. It’s probably more likely that we are going to find him and sell it on a wrap mortgage potentially a contract for deed. Yup. Have we then sold the note at a discount? We haven’t thought that position in our mind not to say you couldn’t, you certainly could, but if we’re going to sell it on our financing, then we’re going to, we’re going to take the long run.

At least in this view that we have right now the long run of, of collecting a monthly payment for the next 25 years or 20 years, whatever it takes.

Yeah. The note sells usually at such a discount that that’s it you have to have huge margins to make it make sense. If you hold up for two or three years, the season usually gets a much better term. If that’s what you’re going to do, or they refinance out of it anyway. Good Terry, thank you so much.

Best lists to find motivated seller leads for creative finance deals (Motivated Seller Lists) [00:35:24]

One of the questions that come up is, is another obvious question is where do you tend to get your creative finance deals from?

I mean, you mentioned in the beginning, that you started calling expired listings. These were expired listings. That’s still a key part of your program. Are there other parts? Are they the same that other people do? Or is there some magic sauce for that?

Funny thing is, this is typically not a lot of magic sauce.

It’s, we’re just, we have different options compared to most other investors out there. And we’re, we’re not so we’re fishing in some of the same ponds, but our conversations are completely different. Expired listings are still a part of our bread and butter. We’re still getting plenty of expired listings depending on the market you’re in. Still doing these for sale by owners, still doing deals.

For rent by owners are fantastic right now with your tired landlords. And then very specific niche lists like high equity, absentee owners, vacant houses all great places. Our properties tend to be the nice move in ready homes Uh, so we’re not dealing in the ugly home space strictly in, I guess you’d consider it like the pretty house space.

How to make more money as a real estate agent using creative finance (Realtor Tips) [00:36:23]

Got it. Got it. I see a question. I know, I know the next step. When you asked, this is asking, do you have a realtor in your group and we’re gonna have 50 people volunteer to be that person.

Is there a realtor in your group, I guess that’s listing the properties or buying the MLS for you or disposing of them.

Yeah. Um, We encourage every one of our associates depending on their market to be communicating and working with realtors. For two different reasons. One is obviously the buyers, the buyers right now, many of you had buyers or realtors had buyers that could qualify that no longer.

And then on the other side is if you have, if you’re coming across properties that you don’t know how to structure the deal, but you know that there’s another route that a seller needs to go, we do give referrals on that end as well.

There was a deal that I typically would show in our presentation, which was a realtor referral, and ends up being, it’s like an $84,000 deal. And we, we do a lot of business with this realtor, but because he was unable to structure the deal he lost about $84,000 worth of income. So I encourage you because we have realtors that are in our group that are now realtor investors, I encourage you to understand the process and be able to offer some of these to your sellers.

So that way you can become more of a one-stop-shop, where it comes, Hey, look, I can list your property and this is what you get, or I can buy your property. And this is what you can get there as well. So you can solve more challenges and be able to build out your portfolio. Those of you that are realtors, wholesalers, or flippers, you are my guess is you’re throwing away deals or coming across potential deals that you just don’t know how to utilize.

And now they’re being passed along to somebody else. So if you just have more tools in your tool belt you could potentially structure. Specifically, because you’re already out there trying to get deals. Right. Sandy asks a question just, just for anybody on this. Are these the sessions recorded and the extras? Yes, probably mastery of the website.

You’ll see all the past sessions. And then I believe this is being live-streamed into the Facebook group as well. Probate mastery has a great Facebook group for you to check out for both of these sessions and ask questions and networking.

Um, you know, I, I always tell people that to be successful, you have to have three things.

It sounds like Zach has it in his program too. You have to have a leader or coach or a trainer or a visionary. I think it’s Probate Mastery that’s Chad… You have to have a kind of system or program or book or methodology that you follow. And I think probably mastery has that through the coaching program.

And it sounds like Zach has it in his program. And the third is you have to have a community, a place where people can work together, share each other’s victories, and encourage each other when there are defeats. Pick them back up again. Game, start again. So probate mastery’s a great resource for all those things, Chad’s there.

I tried to help out as well. You have the probate mastery class, but also you have snippets of it on the website and then also as a group, so feel free to. And pretty mastery Facebook group, or probably master.com. And you’ll see, on the podcast, the past issues, this will be a past issue posted a couple of days.

Okay. For other questions or comments, you raise your hand or put the chatbox where if you’re brave enough, just unmute yourself. Family-style to jump in and I’ll come up here. You have a master real estate investor. Have a few minutes left today. Again, this is Zach Beach. He is the smart real estate coach based in, if you didn’t tell, couldn’t tell in the Northeast wicked smart is a classic term for people from the south Boston area.

Learn creative finance free online; QLS course (Learn Real Estate) [00:39:43]

Can you describe a little bit what, if I was interested in more Zack what’s your program look like? How would I get involved, and where would I find more information? Yeah. Great question. And thanks for asking. We have a couple of different ways to get involved. One, you could always do a self-study.

We have what we call our quantum leap system. Our QLX home study course, where we dive into absolutely everything from how to acquire leads, how to speak to those leads, how to nurture those leads, and how to then structure your deals. Based upon par techniques of owner financing, seller financing, and subject twos, how did then exit your deals with an entire buyer’s process?

We have all the legal documents that you’ll ever need as well. And from there within this program, you can certainly implement every single thing that you would need to implement on day one when it comes to buying and selling real estate without cash, credit, or banks. I did want to make sure that because we were sitting here on this on this, this call here, I w I did want to make sure that I, I gave you guys as much as I could give you.

So we did have a conversation with our team and we were going to give away our entire academy. For you guys as well. So let me just quickly walk you through that. Just I’ll do it in about three seconds here, and then I’ll give you guys a link to go ahead and get involved there, or even just at least get your free free reads here as well.

And Roswell, I’m just going to quickly share my screen with you. So when I look at our course just starts with. Our first mod, which is to, to launch and implement the QoS home study material. My two is, of course, the trackable and predictable systems, and then all the lead generation and lead source you need to, for six to seven figures, mod four has all the scripts running for our students typically do two to four transactions.

How to structure a sign-out deal. We didn’t talk about that today, but you get paid once on the assigned deals. It’s think about it as more or less wholesaling, a lease option contract, and you have the entire module on owner financing, entire module on buying with lease purchases, and selling rent to own.

As you can imagine many of our mentors and people in our space told us why don’t you guys just break apart this course and sell it for thousands of dollars, we’re just not marketers, we’re real estate investors. So we want to make sure you have the entire system. So then sub2, you have your structure sub to deals…

My nine is launching your property and getting home sold and then becoming a transaction engineer, which means how to utilize all of the systems that we’ve talked about there and when to use each option. And then all of our contracts for every single one of the deals that we do. Typically on our course, you’ll see it for 1499.

We follow this genius model, which is exactly what we teach on database, which is mindset, skillset, and your systems. So we did create this entire academy with all of our support products and we wanted to make sure you guys got our entire academy that way you can save tens of thousands of dollars today.

Uh, So those are all of our bonuses that you’ll get included as well. All you have to do is go to smart, real estate coach.com/probate mastery. And it is 497. For you are 497 and $47 a month. And just smart real estate coach.com/probate mastery. Also, we didn’t show you all the free gifts that you guys would get as well.

Just cause we ran this a little bit differently today. If you just go to that same link, you will get all of our gifts there. If so, we want to make sure that if you’re just dipping your toe and you said, Hey, I just want to look at some gifts. Totally get it. You’ll get all of our books.

All my, both of our Amazon best selling books and our deal structure, overtime book, which walks you through all of your deals. You’ll get a free strategy call with us as well. And our micro-course on our tool. Those of you that are serious and want to get involved and want to start implementing this immediately, you’re going to go back to that same link, which is smart real estate coach.com/probate mastery.

You can dive right into the wicked smart academy as well. There is a 30-day money-back guarantee as always. So that would be your best bet to take your next steps when it comes to getting involved in the creative financing space.

Fantastic. And I think the thing that I find is real estate agents, investors will accidentally almost excuse me to sign up for data that they’re going to mail out postcards to, and they’ll get three or 400 leads.

No mail them out. You know, Dollar P is total costs. They’ll melt for six months. It’s a couple of thousand or investment. If we have a chance to even get one deal here, are you talking about a pretty quick investment where you could be doing the subject to within a couple within a couple of weeks, easily falling some of these programs, because they’re going to walk you through the program as part of the academy?

So there is a great program. I’m excited to be part of it offered to you. I’m not involved in the financing part. I’m just here, as a coach and as a participant. Okay. Last questions. I think we cleared them all. I want us to say anything else. I exactly you think I left off that the people that call here are primarily focused already in probate.

They’re calling. People who, who have properties acquired people who have a property to sell some sort. Is there any particular experience and probably that you see the people can take advantage of that, not in terms of your offer, but in terms of, they’re already doing some of the work? As soon as the offers are right in front of them right now, I love they brought this up because last week Chad came on to our community in walk, do walk us through exactly how to utilize probate in order to buy and sell properties through creative financing.

Right. And we’ve had many, conversations with Chad and my father-in-law to create either a, a cohesive product. And I know Chad has been asking us to even bring some of this product into his own space so that way he could offer our course in congruency with the probate, because if you want to have to bring them on someday, but.

I believe one of his first deals with probate was either a lease option, or it was a lease option. So these are, this is set up specifically to work hand in hand. I didn’t bring up probate and our lead sources because the assumption was you guys were already diving into probate cause we’re here in the probate mastery.

So now you have lead sources, many lead sources where you now can offer all these options. And I didn’t mention this, but I mean, our average three paydays for the past 10 years is $75,000 over about 48 months. Little to no money. Now, if you have the ability to structure these deals on top of what you’re currently doing, I’m not saying that to take away anything that’s in your current box and saying to do one at one additional deal a year, two additional deals a year, you saw the $94,000 on, on a 30-month sub to, as you just doing one of those.

How many of those do you need to reach your financial lifestyle, your financial. And it’s a great add-on for those that are already working in the real estate space or those that want to get involved really great risk-averse way to get involved in real estate.

If you’re following Chad, this is the key part of his program.

He’s talked about the importance of these opportunities. As long as I’ve been around him from the very beginning, he talks about his first deal being a lease option. He’ll continue to talk about it the coaching on product mastery in the Facebook group. Feel free to ask questions there. If you guys get involved with the program feel free to continue the dialogue there as well.

Zach, look on behalf of everybody here. I appreciate the energy you brought today and the depth of knowledge and experience you’re able to share with us and the program look forward to seeing more of you and your team here over the months as this kind of partnership with Chad and probably mastery develops.

Thank you so much for being early. Appreciate everybody.

Yeah, thank you very much for having me appreciate it. Humbled, always to come and participate in the group. Take advantage of the free resources along with the paid resources. And I saw some hands that went up feel free to just go to those free resources, smart real estate coach.com/probate mastery, and book that strategy call.

Because then you and I could sit and, and jump on the phone with you and answer some questions as well. If we weren’t able to get to it.

sorry, ran out of time. I found this fascinating. I want here and want to talk about the product that they had enjoyed learning about some of the details. So thanks for bringing so much good information to our group.

I have another call today. This is probably mastery of Chad Corbett’s group. I’m Bill Gross’s substitute today. This calls every Tuesday, noon Pacific 3:00 PM. Eastern, everything in between. It’s live-streamed as well as it’s nicely edited, packaged, and put on the probate mastermind website with all the past episodes. It’s a great source to get information, to add to it.

And then come back to the Facebook group with questions on this other thing. So thank you so much for being with us today. I’m bill gross appreciate you guys. Thank you so much.

Learn more about probate real estate certification and how to find probate real estate opportunities through Probate Mastery